Over the last couple of weeks there has been a shift in the Austin real estate market. You may have seen more open houses, houses that stay on the market longer than they used to and more availability with new builders.

One of the reasons for this is that interest rates have been raised in an effort to slow down / counteract inflation. While it was possible to get an interest rates around 3-4%, they are now sitting North of 5% for primary residence mortgages. What this means that for the same loan amount your monthly payment will be higher for a fixed term (30 years is most common). This can be a difference of a couple of hundred dollars every month, depending on your loan amount and other variables.

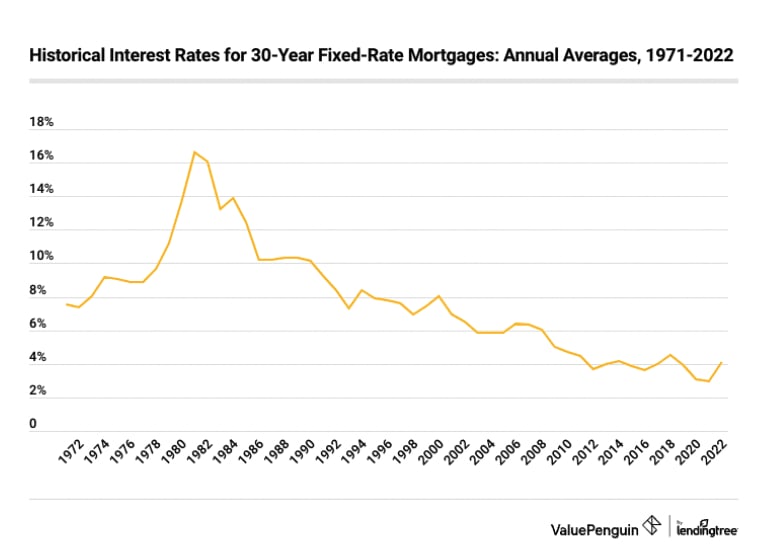

Today's interest rate in context

To put today's interest rate for mortgages into perspective, it helps to look at the historic interest rates over the last 40 years. We have become very used to low rates, but this really has been the lowest we've had in a long time and doesn't necessarily denominate the 'norm'. They first lowered at the end of the housing crash in 2008, and when Covid hit federal fund rates were lowered to 0 - 0.25% resulting in other short-term and long-term rates dropping to help stabilize the economy.

Source: ValuePenguin / lendingtree

What does this mean for home buyers?

With higher interest rates than last year, buying a home now is more expensive. At the same time it's not clear whether interest rates will go down soon or whether they will continue to rise. They will follow the general economic development of the US and historic data shows that there is room for interest rates to go up more. It's definitely worth speaking to a lender to understand what the current interest rates mean to you for monthly payments and decide on whether this is within your budget or not. Buying a house also often depends on other factors like growing a family, moving locations, etc.

There are a couple of things you should consider to bring down your mortgage payment

1. Shop around

You may have a preferred lender, or a lender you have worked with in the past, but make sure to shop around for the best conditions for you. There is a difference between local lenders or credit unions and bigger banks and they may all come with a different fee structure.

2. Increase your down payment

The higher the down payment, the lower the loan amount and the lower your monthly payment. You'll see the biggest jump at 20% down payment as this will remove the need to pay PMI (private mortgage insurance) which costs around 0.5-1.5% of the loan amount per year.

3. Consider buying mortgage points

This basically is an upfront payment of a lump sum to reduce your interest rate. The monthly costs are lower, but keep in mind that you will need to bring more cash upfront and it will take some time for you to break even between the upfront payment and savings in monthly payments. Generally speaking this makes more sense if you are planning on owning your home for a longer time.

4. Refinance your mortgage

This makes sense if your credit score has improved or rates have gone down. Keep in mind that there is a cost involved with refinancing (which will be worked into your mortgage). As mentioned above, make sure to shop around for the best conditions.

5. Work on your credit score

It is possible to get a mortgage with credit scores around 650, but they will typically come at the higher end of the interest rate range. Increase your credit score and chances are that you'll move towards the lower end of that range!